Where are we on Ethereum’s roadmap?

2022 was all about the Merge as Ethereum successfully transitioned from Proof-of-Work to Proof-of-Stake with the Paris upgrade. On 12 April, Ethereum is set to undergo the Shanghai and Capella upgrades, which will enable withdrawals of staked ETH, thereby fully transitioning Ethereum into a PoS blockchain.

In this article below, we will share the background of “Shapella”, what it means for the price of $ETH, who the winners are, before shedding light on what’s next on the Ethereum roadmap.

Background of Shapella

While Shapella seems to suggest a singular change to Ethereum, it is actually a name coined from the two different upgrades that will take place simultaneously with the fork — Shanghai and Capella. Ethereum’s execution layer will undergo the Shanghai upgrade, while its consensus layer undergoes the Capella upgrade.

While there are five EIPs that form the Shanghai upgrade, the most significant one is EIP-4895. It enables withdrawals of staked ETH, including all ETH that has been staked and locked in Ethereum’s consensus layer (the Beacon Chain) by validators since its launch in December 2020. Capella, which marks the third major upgrade to the consensus layer, serves to facilitate this, not only allowing blocks to process withdrawal requests but also implementing an account sweeping function that we will elaborate about later on.

Once both the Shanghai and Capella upgrades are complete, ETH withdrawals will then happen in two ways — full and partial.

Partial Withdrawals

A partial withdrawal only entails the amounts in excess of the 32 ETH required to run a validator. This account sweeping (or ‘skimming’) happens automatically and periodically for any active validators that have updated to the new withdrawal credentials.

This serves as an extremely useful feature for two key reasons:

- As validator rewards do not auto-compound, this mechanism serves to increase the capital efficiency of stakers’ funds. Stakers will be allowed to redeploy their excess ETH for other yields, all without having to incur any gas costs.

- Partial withdrawals prevent long exit queues and excessive validator churn, which would otherwise be the case if validators were required to completely exit the Beacon Chain to access their rewards, potentially destabilising the network.

Since only 16 partial withdrawals will occur every slot, the frequency of skimming is heavily dependent on the total number of eligible validators. Validators should expect a range of 2–5 days between partial withdrawals.

Full Withdrawals

A full withdrawal happens if a validator chooses to completely ‘exit’ its position as an active validator of the network, thereby reclaiming its entire balance, made up of the original 32 ETH and all rewards accrued since its inception.

Similar to other PoS blockchains, a validator will have an unbonding period where they will have to wait before receiving their entire balance of stake and rewards. The length of this unbonding period is determined by the sum of two variable times — the time it takes for a validator to exit Ethereum’s consensus layer and the time it takes for the entire withdrawal process. Validators looking to make a full withdrawal should therefore expect a minimum of 261 epochs, or 28 hours.

Another variable to factor is the churn limit. This defines the maximum number of validators that can be exited from the consensus layer in each epoch, which increases with the total number of active validators. With ~525K validators today, around 8 exits are permitted per epoch, which translates to a maximum of 1.8k validators exiting per day. Consensys goes into great deal of how these estimates are achieved here.

What does this means for the price of $ETH?

With over 18m ETH staked on the Beacon Chain to date, it becomes clear why the months leading up to the Shapella upgrade have been plagued with uncertainty and worry amongst investors. At a surface level, the enabling of withdrawals should cause a supply shock that leads to significant downwards pressure on the price of ETH. But what could the actual impact be?

The state of existing ETH stakers

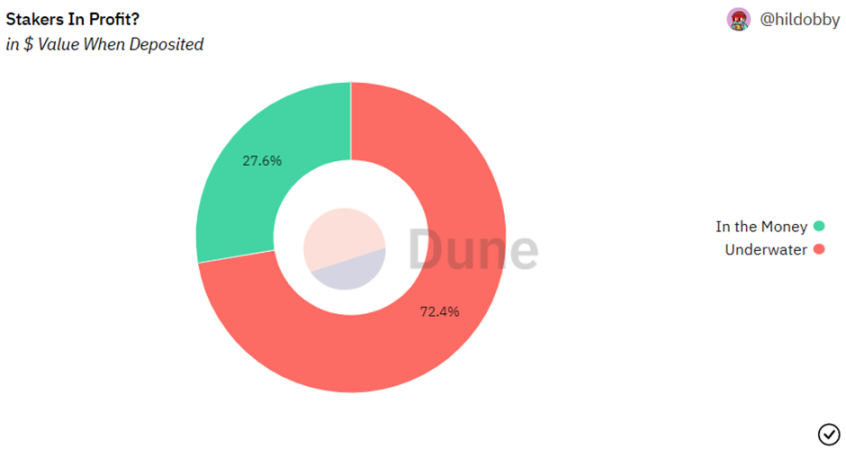

To make an estimate on the potential price impacts, we need to first assess the state of existing stakers and the decisions they might take. We believe these decisions will be largely driven by the financial situation of the stakers. In other words, are ETH stakers in the money or underwater from their initial staking?

A dashboard done by hildobby reveals that only 27% of ETH stakers are actually in the money based on the dollar value of their assets, leaving a whopping 73% underwater. This fact alone might already serve as a deterrent and disincentive for current stakers to dump their retrieved ETH and effectively realising their losses, and instead restake their accumulated rewards and maximise their yield going forward.

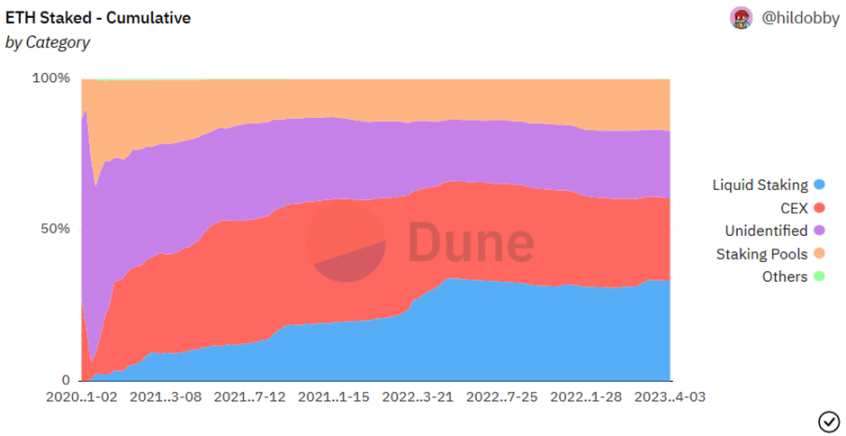

Amount of stake with Liquid Staking Protocols

Another factor would be the consideration of how much ETH has already been staked via liquid staking protocols (LSPs). At the point of writing, this number is above 30% (closer to 45% when including Coinbase, according to DefiLlama), with the majority coming from Lido.

In the case of Lido, stETH rebases automatically to factor in accumulated rewards from liquid staking. This means that users who chose to stake with Lido could already “realise” their ETH rewards by selling on the secondary market, should they wish to do so. Therefore, there should be less direct withdrawal pressure on the validators behind Lido, who should retain some flexibilty over what they wish to do with the excess rewards.

We believe that these validators would put these excess rewards to better use, by expanding their validator sets instead of selling. Therefore, this further downplays the overall downwards pressure that the enabling of ETH withdrawals and influx of ETH will have on its price.

The price of $ETH

Now that we considered the key factors that determine the potential supply of ETH rewards that could be sold, what does it mean for the price of $ETH?

“If we assume that validators will sell 50% of their staked ETH rewards (not their principally staked ETH), we expect 553,650 ETH will be sold. Amortized over 7 days, this amounts to approximately 1% of daily ETH volume (including spot and perpetual futures volume) of selling per day for a week.

Depending on the risk environment broadly and overall liquidity in Ether during the Shanghai upgrade, expected in early April, we view this amount as ranging from inconsequential to slightly bearish ETHUSD. Another view is that the Shanghai upgrade going smoothly is broadly bullish for Ethereum as a technology, and thus bullish for ETHUSD.” — Galaxy

While are unable to provide price predictions, we would like to share the viewpoint from Galaxy who wrote an amazing article exploring the potential outcomes based on the amount of partial and full withdrawals executed and we highly recommend a read.

Regardless of where the price ends up, we believe that Shapella will unlock new opportunities within Ethereum which we share below.

The winners of the Shapella Upgrade

Liquid Staking Protocols

The Shapella upgrade will likely be a bullish catalyst for Liquid Staking Protocols (LSPs) for a multitude of reasons.

- With ETH withdrawals enabled, it should be easier and more cost-efficient for LSPs to maintain the peg between their respective Liquid Staking Derivatives (LSDs) and ETH. This makes LSDs better borrowing collateral since the tighter peg helps limit price volatility and therefore lowers liquidation risks. Combined with the increasing adoption of LSDs within Ethereum’s DeFi ecosystem, this becomes an extremely attractive opportunity for investors to pursue more capital efficient yield farming.

- The tighter peg also promotes the liquid staking of ETH as a more ‘risk-free’ or benchmark rate for investors, who were once wary of the maintenance of the peg being largely dependent on the balancing of demand and supply of various liquidity pools, which failure is very much still within recent memory (stETH depeg due to massive selloffs on Curve).

For these reasons, we expect both a majority of retrieved ETH from full withdrawals and sidelined ETH to flow into LSPs, and for their adoption to further increase. But are some LSPs primed to fare better than others? We run through the some of the different LSPs and their vast range of features below, from flywheels and feedback loops, giving users more control over their withdrawal keys, utilising NFTs, to employing MEV strategies for extra yield.

Lido Finance (LDO, stETH)

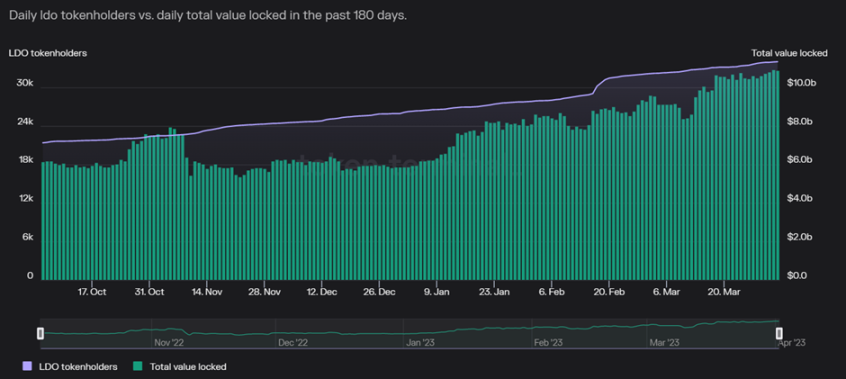

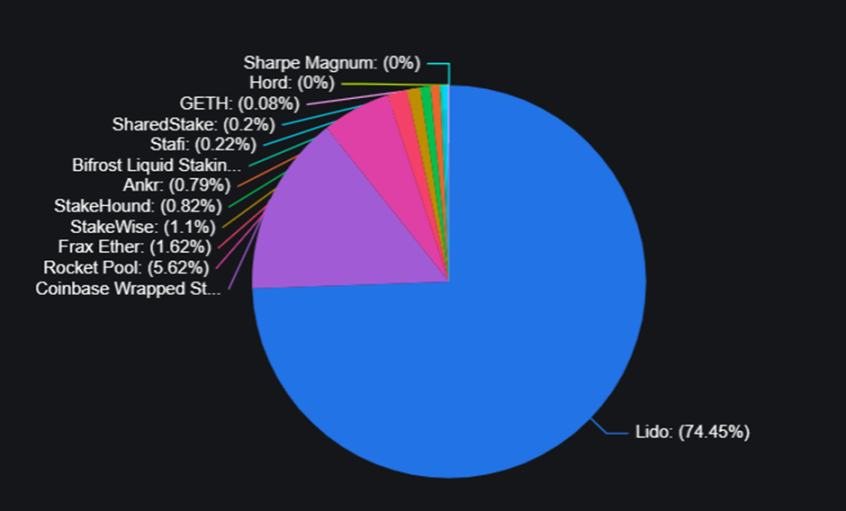

Having establishing itself as a market leader within the LSP space, Lido seems to be a clear bet when it comes to increasing its TVL after the upgrade. With a strong reputation, deep liquidity, and the most integrations within DeFi, there is a strong case for users in search of liquid staking services to choose Lido. This is evidenced by Lido’s number of token holders and TVL being on an upward trend since November, contributing to almost 75% of the total staked ETH to date.

With centralisation concerns over Lido’s dominance, coupled with increased scrutiny over governance after the Arbitrum incident, their governance system will play an important role more than ever. While it should be applauded that they have taken steps to include stETH holders as part of governance with LDO holders, users who want to help out with decentralisation of stake on ETH can also consider other alternatives we listed below. Lido had also recently announced that its upcoming v2 will be a step towards further decentralisation and centered around two major upgrades — withdrawals and the staking router.

Swell Network

Swell Network is also an upcoming LSP that aims to provide higher staking yields to users. Currently live with their latest version Seawolf on Goerli testnet, Swell is preparing for a launch on Ethereum mainnet in late April following the Shapella upgrade. While operating with a permissioned group of professional node operators initially to provide the scale, reliability and yield to users in a competitive environment, subsequent iterations will see the operator set expand and ultimately be permissionless with enough liquidity, stability and with risk mitigation technologies like DVT, in line with the protocol’s values.

swETH, the liquid staking token of Swell will be a reward bearing token that increases in value as rewards accrue on chain. Users can expect to receive rewards in the form of consensus layer rewards (e.g. Staking yield) and execution layer rewards (e.g. Priority fees and MEV). Stakers with Swell Network can also access vaults that run yield-boosting strategies all within their dApp. Swell will launch as the lowest cost staking option on the market, with no protocol staking fees.

Rocket Pool (RPL, rETH)

While Rocket Pool seems to have advantages over other more dominant players like LDO with its more decentralised node operator network and lower capital requirement of 16 ETH to run nodes, it does have its fair share of drawbacks. These include a higher performance fee vs competitors, and the collateral requirement that node operators must lock a percentage value of their staked ETH in RPL as collateral for protocol insurance.

Despite this increased friction for users looking to operate nodes out of Rocket Pool, the perks of the upcoming Atlas upgrade might just prove to be sufficient enough to outweigh it. The Atlas upgrade, planned for 18 April, brings about several improvements including increased protocol efficiency, higher node operator rewards, and greatly boosted rETH capacity while retaining the protocol’s fully permissionless nature. One of the most significant features is the introduction of 8 ETH minipools which will bring the minimum capital requirements even lower. At the same time, this feature results in greater returns for both the node operator and rETH stakers, providing up to 18% more rewards when a user runs two 8-ETH minipools instead of one 16-ETH minipool. While this bodes well for Rocket Pool’s future, we will still need to observe if the update is truly effective in siphoning away both TVL and market share from its competitors once implemented.

Frax Finance (FXS, frxETH/sfrxETH)

Having seen the largest relative growth in staked ETH this year, Frax also proves to be a strong contender in the coming future. This growth is easily linked to the fact that Frax offers the highest staking APR of all LSPs at around 5.6%, sustained through its dual token model. For background, frxETH acts as a stablecoin that is loosely pegged to ETH and sfrxETH is the staked version of frxETH that earns staking rewards. With this design, Frax enables frxETH holders to generate yield in multiple ways — staking to receive sfrxETH and validator rewards, or providing frxETH-ETH liquidity on Curve. These two options work together to create not only deeper liquidity for frxETH but also higher APRs in sfrxETH and the Curve liquidity pools.

Like Rocket Pool, Frax also has an upgrade planned for post-Shapella that might serve as a strong catalyst for its adoption. The frxETH v2 upgrade is planned to increase decentralisation through enabling permissionless validators, instead of limiting them to ones that are run by the protocol itself. Besides this, a recent proposal to utilise FXS bribes and incentives to bootstrap liquidity for future frxETH trading pairs has been passed, creating a strong flywheel that, in theory, ultimately results in an increase in value of FXS and the supply of frxETH, and a positive feedback loop that generates higher yields and attracts more liquidity for the LSD. DWF Labs’ ZhouYeMen covers this topic in great detail and with great understanding here.

Ether.fi (eETH)

While Ether.fi is yet another decentralised LSP to enter the market, it has some major differentiating characteristics. These include the fact that it is a non-custodial delegated staking protocol where stakers generate and hold their own staked ETH keys, and its utilisation of NFTs, minted for every validator that is launched via the protocol. These NFTs control the 32 ETH staked, and store metadata related to the validator — the client it runs, the geography it is in, the node operator, and any node services it is running. Ether.fi’s LSD eETH is then minted from a liquidity pool containing these NFTs.

The combination of these two mechanisms allow for stakers themselves, to submit exit commands for validators instead of the usual node operators. The recovered staked ETH is then deposited into a withdrawal safe, where stakers will be able to recover their ETH net of fees through the burning of their NFTs. This successfully reduces stakers’ exposure to significant and opaque counterparty risks present with other LSPs and at the same time, ensures that there will always be sufficient ETH liquidity for eETH holders to redeem. Therefore, we expect Ether.fi to be one of the upcoming LSPs to see an influx of users and TVL post-Shapella.

In the future, Ether.fi plans to leverage EigenLayer to create a node services marketplace where stakers and node operators can enroll their minted NFTs to provide node infrastructure services, with the revenue from these services being shared with stakers and node operators. Currently, Ether.fi already offers institutional staking services that can accommodate bespoke investment structures, alongside an early adopter program for its retail-facing liquid staking. With ETH withdrawals enabled, it is possible that institutions will look to ETH staking as a viable investment as well, and Ether.fi is positioned to be one of the many beneficiaries.

Manifold Finance (FOLD, mevETH)

Like Ether.fi, Manifold is a newer entrant to the LSP scene, introducing its MEV-optimised, natively multichain LSP less than a week ago. Its LSD mevETH is implemented as an omnichain fungible token (OFT) that makes it antively bridgeable across chains without the need for wrappers, potentially making it the most composable LSD to date. At the same time, mevETH is designed around MEV capture, employing novel and unique MEV approaches only available to Manifold’s LSP, offering holders extra yield on top of staking yields. One such approach has been revealed to be arbitraging the peg between ETH and mevETH, not only acting as a means to provide extra yield, but also to strengthen the peg.

Manifold has indicated their goal to accumulate 100K ETH by the end of the year, around a sixth of Lido’s current staked ETH. As LSDs are slowly integrated into existing DeFi protocols, mevETH’s high composability might serve to propel it to the forefront of adoption, carving out a strong portion of market share for itself.

Regardless of which protocols end up benefitting the most from the Shapella upgrade, it is almost definite that we see an increase in overall ETH staking participation due to the increase in attractiveness of liquid staking, whether due to a naturally stronger peg or protocol-led developments. Based on staking ratios of other PoS chains like Polygon and Solana, ETH staking ratio seems likely to increase towards the range of 40–70%, up at least 2x from the current 15%. While this might raise concerns of eventual lower staking yield and greater supply inflation, this opens up many other opportunities and possibilities, which we will now explore.

DeFi

As covered above, LSDs are set to become more prevalent in increasing stake participation for Ethereum. With withdrawals enabled, LSDs can maintain a tighter peg with ETH which then reduces volatility and make LSDs better collateral, all while generating yield. Below are a few protocols that are taking advantage of the increased adoption of LSDs and their opportunity for greater capital efficiency in the form of leverage.

Pendle Finance (PENDLE)

Pendle is a yield-trading protocol, allowing users to execute various yield management strategies by wrapping yield-bearing tokens and splitting them into 2 tokens — PT that represents the principal, and YT that represents its yield, that can both be traded via their custom AMM. 1 PT gives holders the right to redeem 1 unit of the underlying asset upon maturity, a date decided on by the initial tokenholder, while 1 YT gives holders the right to receive yield on 1 unit of the underlying asset until the same date of maturity. This allows Pendle to essentially create a market for yield, enabling users to adopt multiple strategies including longing assets at a discount, longing yield APY, and even obtain a fixed yield for low-risk and stable growth.

Likewise, staked ETH holders are able to utilise Pendle to split each of their stETH, for example, into 1 PT stETH and 1 YT stETH, then leveraging Pendle’s custom AMM to trade either asset and make directional bets on yield too. With the upcoming Shapella upgrade and expectations of staking yield falling over time, one possible trade stETH holders could take taking the opportunity to sell YT stETH at current prices based on its existing yield, profitting the difference between stETH’s current and future yield.

Since December, Pendle has already experienced a 7x spike in TVL, with more and more users discovering its potential. A breakdown of tokens within its TVL according to DefiLlama, also reveals more than a third being attributable to LSDs, including stETH and frxETH.

With Pendle’s latest integration of sfrxETH, it is likely that we will see an increase in the LSD’s dominance within Pendle’s TVL. Similar to what has been done with stETH, Pendle allows for the LPing of PT sfrxETH that returns up to 99.2% boosted APY with zero exposure to impermanent loss, achieved through a balanced strategy of fixed yield exposure and native yield, complemented by swap fees and PENDLE emissions.

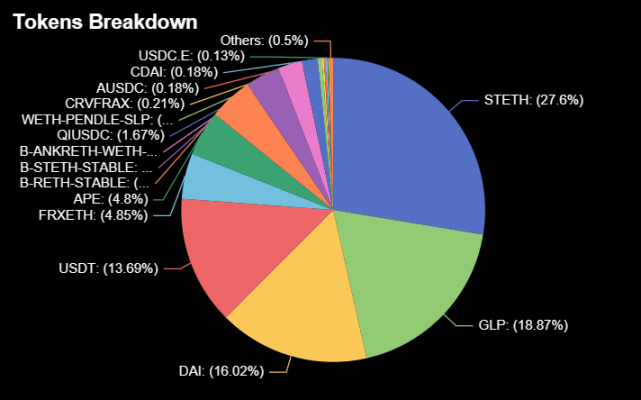

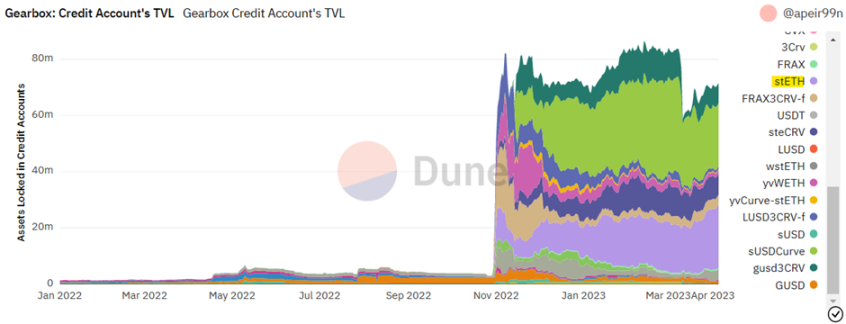

Gearbox (GEAR)

On the topic of leverage, the tighter peg between LSDs and ETH after the Shapella upgrade as mentioned above, unlocks the viability of leveraged ETH staking, due to the lowered risk of liquidation. Gearbox is a two-sided lending marketplace that connects users looking to supply their assets for a passive and safe APY with leverage lovers who seek the extra capital to do so. The protocol introduces leveraged liquid staking derivatives, or LLSDs, as a single-click strategy for users to natively stake up to 10x the value of their collateral in ETH to earn greater staking yield, churning out up to a maximum of over 12%, compared to the 4.3% APR currently offered by Lido.

To date, this strategy is enabled for both Lido’s stETH and Coinbase’s cbETH (waiting on DAO vote), with plans to integrate both frxETH and rETH from Frax and Rocket Pool respectively once they have mainnet Chainlink oracles available. By acting as a base layer of leverage, Gearbox is positioned to indirectly benefit from the expected increase in the amount of ETH staked, and the increased growth and adoption of LSPs and LSDs, as more ETH stakers look for relatively low-risk methods to increase their staking yield. This has already seen significant adoption in the past few months, with stETH accounting for more than $22M or a third of Gearbox’s total Credit Account TVL.

With the launch of Gearbox v3 being on the horizon as well, one can expect new features such as automated portfolio management and health factor maintenance to further incentivise LSD token holders to utilise Gearbox’s leverage capabilities, propelling it to the forefront of DeFi.

Flashstake (FLASH)

Flashstake is another novel protocol that introduces a unique mechanism to increase capital efficiency on users’ assets. Users deposit and stake their assets, locking in current yield APRs and minting time-based derivatives (TBDs) that correspond to their position. Users can then burn or swap these TBDs to claim upfront yield on their assets, reclaiming their principal deposit after the chosen staking period. This is particularly interesting given the expectation for ETH staking yield to decrease over time. Flashstake enables early users to not only secure and fix the current (and supposedly highest) ETH staking yield for a maximum period of 1 year, but also continue generating yield on their rewards elsewhere.

Understandably, this might raise some eyebrows. Where exactly does this upfront yield come from? To provide this yield to users, Flashstake employs a 3-pool approach that comprises of Yield Pools, Liquidity Pools and Boost Pools.

Unlike loans, Flashstake’s pool-based approach also ensures that user’s deposited assets are always 100% collateralised and do not face any risk of liquidation. The isolation of each vault strategy also serves to provide an additional layer of security for users since the effects of any potential exploits are kept within the compromised vault. With a strong value proposition featuring a novel mechanism, alongside strong security elements, Flashstake’s TVL seems well-poised to benefit from the influx of liquid ETH and increased adoption of liquid staking.

Restaking

EigenLayer

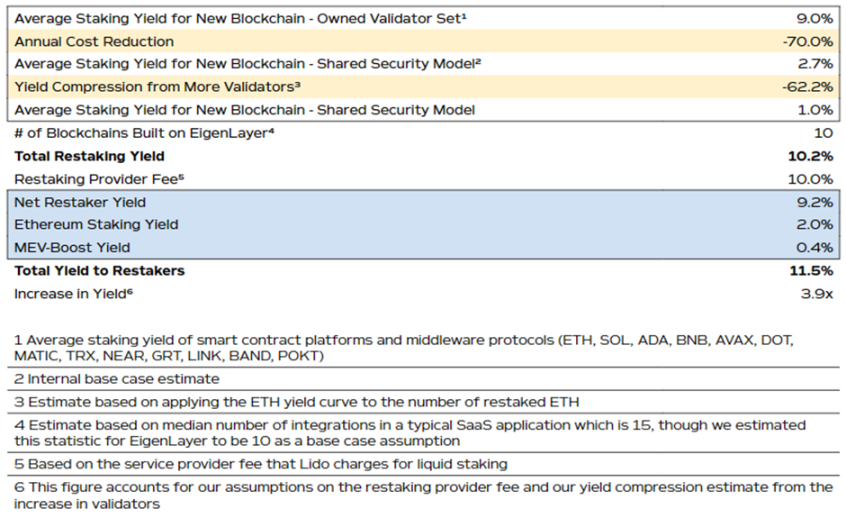

With withdrawals now available, ETH that are staked with EigenLayer contracts can be withdrawn and slashed if malicious intent is detected. This paves the way for EigenLayer to become the decentralised trust layer for applications to build upon where existing ETH stakers can opt in to secure new applications on EigenLayer with their stake. EigenLayer’s restaking mechanism provides users with an incremental yield opportunity on top of what they would receive through plainly staking their ETH and receiving MEV-related rewards, while serving its primary purpose of modularising Ethereum’s trust layer and enabling a broad design space for new middleware and adjacent chains to launch.

Finality Capital Partners projects ETH restakers to earn up to 11.5% APY by 2028, up from a forecasted baseline ETH staking yield of 2.0% or so in 2028. The 2.0% staking yield is based on their expectations of the ETH staked ratio, which they believe could be 60%, up from the current 15%. Their full report on EigenLayer and restaking can be found here. As such, we see restaking via EigenLayer becoming commonplace for ETH stakers, especially those looking for a relatively lower risk method to increase their yield.

New Primitives

Ion Protocol

Despite somewhat successful efforts to increase adoption of LSDs in DeFi, there is still huge friction in doing so. With a multitude of different LSDs and liquid staking designs, DeFi protocols looking to integrate each of them would need multiple bespoke and novel solutions. For example, Uniswap is unable to accept rebasing LSDs such as stETH from Lido, while blue-chip protocols such as Aave and Maker need to create separate vaults and pools for different LSD tokens. This leads to fragmented and shallower liquidity for LSDs, therefore resulting in increased slippage and inefficient price discoveries, defeating their very purpose of representing staked ETH and distributing staking yield.

Amongst its many goals, Ion Protocol aims to utilise a dual-token model to aggregate deposits of various existing LSD tokens into a universal unit of account, providing a solution to the above stated problem. This universal unit of account would allow better frictionless integration into DeFi, tapping into the full potential of LSDs being utilised as low-risk, yield-generating collateral, or even greater capital efficiency through leverage.

UnshETH (USH)

UnshETH is a decentralised, unchain movement that aims to solve this problem, promoting validator decentralisation through incentives, directing more yield to LSPs and LSDs with lower dominance. This is done through a new class of primitives, termed LSDfi, including Validator Decentralisation Mining (vdMining) and Validator Dominance Options (VDOs).

vdMining is a token distribution mechanism that rewards users the more they stake with LSPs that align with a predefined optimal decentralisation ratio, and VDOs are a mechanism that allows holders of a dominant LSD to sell “puts” on their validator dominance percentage, with the strike price set at a lower percentage than their current dominance. If at expiration the dominance falls below the strike price, the VDO holder loses a portion of their yield, which is distributed to holders of other LSDs. These two mechanisms combine to incentivise new stakers to do so with less dominant LSPs, and more existing dominant LSD holders to diversify their capital into various LSPs.

Plans for new features following the Shapella upgrade are also in place, these include a router for staked ETH liquidity and others that serve to increase the utility of UnshETH’s native token USH. It will be interesting to see just how large a TVL UnshETH will eventually capture as it spearheads a new primitive and works towards its goal of decentralising validators as staking becomes the de facto yield farming solution for ETH holders.

Zero Liquid (ZERO)

Zero Liquid is another emerging protocol that could fall within the new primitive of LSDfi, issuing self-repaying loans for users’ LSDs. Similar to more traditional money market protocols like Aave, Euler, and others, users first deposit assets as collateral and then are able to take out loans at a fraction of their collateral’s value.

In Zero Liquid’s case, users are able to deposit LSDs and native chain tokens (ETH, MATIC, etc.) as collateral, receiving a synthetic version of the asset as a loan. However, some distinguishing factors of these loans are their 0% interest and self-repaying nature, which combined with the use of a synthetic asset, allows the protocol to provide a zero liquidation model. To achieve this, Zero Liquid utilises the yield generated from a user’s deposited collateral to automatically pay off their debt.

While the protocol has yet to officially launch its product, one can already foresee the many unique use cases outside of maximising a user’s assets, in which it comes in extremely handy. With Zero Liquid, users would essentially be able to make investments and purchases without the requirement of any upfront capital. Drawing some similarity to the real world’s Buy Now Pay Later model, payment through Zero Liquid’s product would allow users to make purchases or ‘spend’ now and pay only with the future yield of their deposited collateral (or time, depending on how you see it).

Just like UnshETH, Zero Liquid introduces a completely new model and mechanism to solve existing problems that users face, at the same time unlocking the potential and increasing the use cases of LSDs. Still being in their infancy, both these protocols have much to prove in terms of PMF and their actual ability to attract users to achieve what they set out to, but it is no question that these new developments present an even more bullish case for LSDs.

What’s next after Shapella?

After Shapella, the next exciting upgrade to Ethereum will be the Cancun fork, which forms part of the scaling roadmap. While L2s such as Optimism and Arbitrum have reduced costs over 8x that of Ethereum base layer, data storage has always been the bottleneck in terms of cheaper transaction fees, making up over 90% of the transaction costs.

EIP-4844 aims to reduce the cost of L2 rollups by 10–100x and usher in a new era of low-cost onchain activity. This is done by introducing proto-danksharding to Ethereum, implementing most of the logic and “scaffolding” (e.g. transaction formats, verification rules) that make up a full Danksharding spec. By introducing temporary ‘blob’ storage that can be deleted from Ethereum once they are no longer needed, it is expected to provide a >100x increase to throughput and reduction in transaction costs to the tune of <$0.001.

Other improvements that could be included in the Cancun upgrade are EIPs within the EVM Object Format (EOF) group. These are six EIPs that have accumulated over the years, all intending to better structure bytecode, or computer object code that an interpreter converts into binary machine code so it can be read by a computer’s hardware processor, to make the system faster, more efficient, cheaper, and safer. One has already been included in the previous London upgrade, and some within the coming Shanghai upgrade, with the remaining likely to come with Cancun. This will serve for the implementation of EOF2, a new EOF extension that overhauls control flow.

The immediate beneficiaries of the Cancun upgrade will be the production-ready rollups and its users, who should see transaction costs come down significantly. Second order effects could be new applications and primitives that could take advantage of the upgrades, such as on-chain order books given costs are now cheaper, or even decentralised physical infrastructure networks that could utilise faster transactions on L2 while settling onto the trusted Ethereum base layer. We will look to dive deeper into these opportunities as we get closer to the Cancun upgrade.

Disclaimer: Bixin Ventures are investors in EigenLayer, Pendle Finance, and Swell Network that were mentioned in this article.

Article Contributors: Henry Ang, Mustafa Yilham, Allen Zhao, Jermaine Wong & Jin Hao

【免责声明】市场有风险,投资需谨慎。本文不构成投资建议,用户应考虑本文中的任何意见、观点或结论是否符合其特定状况。据此投资,责任自负。